The latest from Marvin

The Global Biofuel Boom: A Strategic Moment for Brazilian Bioenergy Producers

Global biofuel demand is shifting. Governments are raising blending mandates, transport decarbonization targets keep tightening, and fuel buyers are looking for larger volumes of certified low-carbon ethanol.

Biofuels are becoming a larger part of the global energy mix

Bioenergy is already the world’s largest source of renewable energy, accounting for more than half of global renewable energy consumption according to the International Energy Agency (IEA). Demand continues to accelerate across transportation, aviation, and industrial fuel markets.

The IEA’s Renewables 2025 report projects that liquid biofuel consumption will rise from 2.3 to 6.0 million barrels of oil equivalent per day by 2030, representing growth of more than 160% over the period. Bioenergy is expected to account for most renewable fuel expansion globally during the decade. This growth is being driven by regulation as much as by market demand.

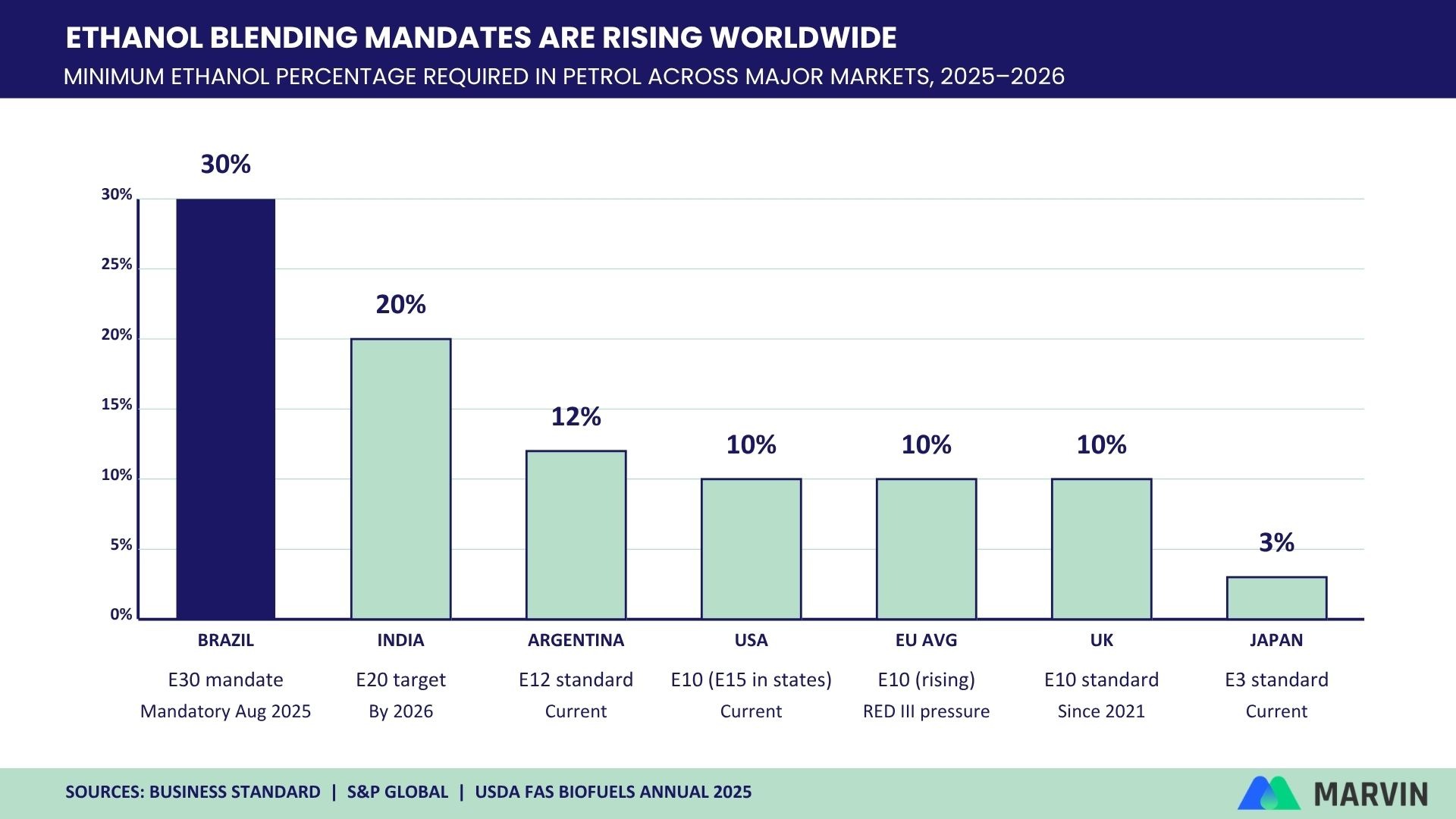

Countries are increasing mandatory biofuel blending requirements as part of broader emissions reduction strategies. These mandates directly affect fuel consumption volumes because they require gasoline and diesel distributors to include minimum percentages of renewable fuels within the national fuel mix, as the chart below shows.

Brazil implemented E30 in 2025, raising the ethanol blend in gasoline to 30%, with discussions around E32 already underway. India continues advancing toward E20 adoption across most of its fuel market. The European Union is tightening renewable fuel requirements under RED III, while the United States maintains E10 to E15 blending levels under the RFS framework.

Even relatively small mandate increases translate into substantial additional fuel demand. Brazil’s transition from E27 to E30 alone added an estimated 2 to 2.7 billion liters of annual ethanol demand.

Europe’s tightening renewable fuel market is creating a favorable environment for Brazilian exports

Europe’s renewable fuel market is relying more heavily on imported ethanol. The European Commission expects renewable ethanol demand to continue growing through 2030 as member states implement RED III targets. At the same time, European supply conditions tightened during 2025 amid lower production and stronger mandate-driven demand.

According to Argus Media, European ethanol prices reached multi-year highs during 2025 as market participants responded to tightening supply conditions and stronger mandate-driven demand.

Brazil enters this market with two structural advantages.

The first is production scale. Brazil maintains one of the world’s largest ethanol industries, supported by mature sugarcane infrastructure and relatively low carbon intensity production. The Center-South region closed the 2025/26 harvest with approximately 611 million tons of processed sugarcane while maintaining strong ethanol output.

The second advantage is trade access. The Mercosur-European Union agreement entered provisional application in May 2026 and established preferential tariff quotas for Brazilian ethanol exports into the EU.

For European fuel buyers, Brazilian ethanol increasingly represents one of the most commercially viable sources of imported low-carbon fuel.

A Time-Sensitive Opportunity for Brazilian Ethanol

Current market conditions create a relatively narrow but attractive export window for Brazilian producers.

The United States still remains an attractive destination for renewable fuels under the RFS framework, although future changes in credit treatment for imported feedstocks may gradually reduce some of that advantage after 2027.

For Brazilian producers, the current combination of European demand growth and still-favorable export economics creates a rare commercial window across multiple regulated fuel markets.

Decoding Biofuel Certification Requirements

As international biofuel trade expands, certification requirements are becoming more directly tied to commercial competitiveness.

European fuel markets increasingly require verified greenhouse gas reductions, feedstock origin documentation, land-use compliance, and auditable chain-of-custody systems. Standards such as ISCC EU have become central to market access under RED III, while Bonsucro continues gaining relevance within sugarcane supply chains.

This shift is already affecting trade flows. Between 2022 and 2025, U.S. ethanol exports to the European Union increased substantially while Brazilian exports declined. Certification readiness and compliance alignment became important differentiators between suppliers competing for access to European markets.

Managing these requirements becomes operationally complex for producers handling multiple certifications simultaneously. Emissions calculations, supplier declarations, transaction records, audit evidence, and traceability documentation are often distributed across disconnected systems and manual workflows.

Building certification readiness at scale

For producers exporting into regulated fuel markets, certification management is increasingly becoming part of operational infrastructure rather than a periodic compliance activity.

Marvin centralizes ISCC, Bonsucro, RSB, and RenovaBio requirements within a unified audit-ready system. By consolidating supplier data, emissions records, traceability documentation, and certification evidence in one environment, companies can manage multiple frameworks without duplicating operational effort.

The producers best positioned for the next phase of ethanol trade will be those combining production scale with verified, traceable, certification-aligned supply chains.

Our Latest Resources

Why AI Agents Are the New Architecture for Global Supply Chain Arbitrage

The EU Packaging and Packaging Waste Regulation (PPWR), requires companies selling packaged goods in the EU to prove the origin, composition, and recyclability of their packaging, turning compliance into a supply-chain data challenge.